Nothing says summer like racking up debt. Plus, we take a look at credit card and student loan debt to ask who's benefiting from loan relief? And, is financial literacy an excuse for lazy thinking?

The average asking rent across all unit types in May was $1,832. The median was $1,716. All types had a modest uptick in asking price, which is consistent with a hotter summer rental market. This is the second month data from our new code is showing a positive skew, with a handful of luxury units (about 2 – 3% in each category) pushing the average up.

Studio: $1,410 Average | $1,450 Median

1 Bedroom: $1,617 Average | $1,606 Median

2 Bedroom: $1,759 Average | $1,700 Median

3 Bedroom: $2,238 Average | $2,200. Median

4+ Bedroom: $2,716 Average | $2,695 Median

(n=4027)

Credit Card Debt

I recently had the privilege of giving a guest lecture on the financialization of housing at McGill University, my old PhD haunt. In class, a student asked about the rise of Klarna, a kind of pay-as-you-go service that lets you put pretty much anything on layaway, from airline tickets to a cup of coffee. I heard that use of things like Klarna was on the rise, as were customer defaults. In fact, defaults on credit of all kinds are up. U.S. credit card debt hit a record high of $1.17 trillion in the third quarter of 2024, up from $770 billion in early 2021. At the same time, the share of card holders making only minimum payments climbed to 10.75%. That’s the highest level since 2012.

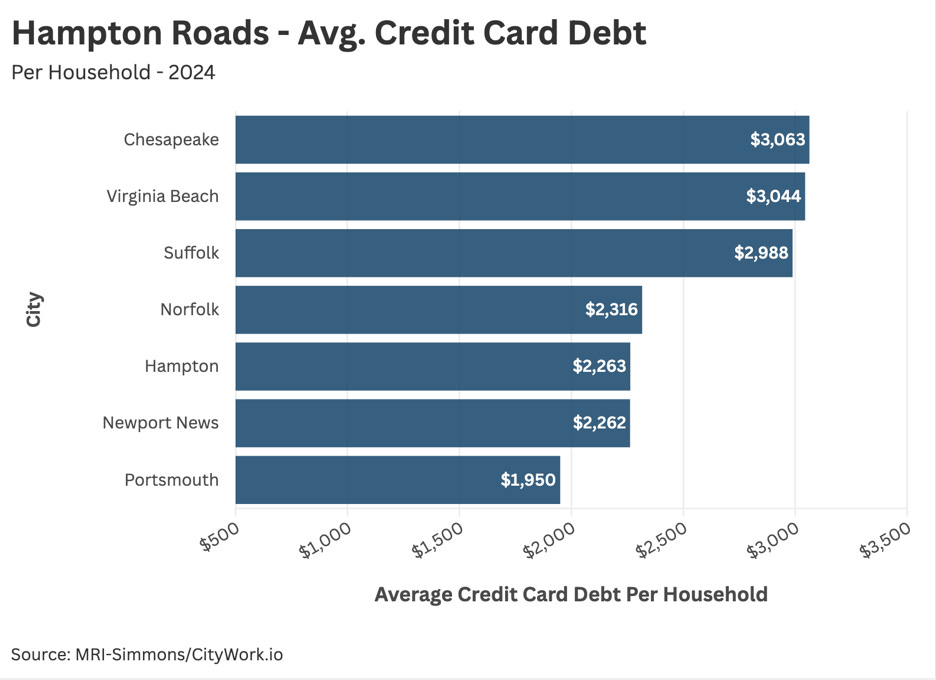

So what does credit card debt look like in Hampton Roads?

Chesapeake and Virginia Beach have the highest average credit card debt per household, which isn’t surprising given that wealthier homes tend to spend more.

In terms of changes, from 2022 to 2023, credit card debt crept up modestly, about $28 per household. But from 2023 to 2024, Households pulled back sharply, cutting average balances by roughly $320. Overall for the region, credit card debt dropped by nearly 10% from 2022 to 2024, with households across the region averaging cuts by roughly $320, bucking a national trend.

One way to interpret the uptick then reduction, in the context of a high-inflation environment, is that households were leaning on credit cards during a period of peak hardship and then eased off. I don’t necessarily buy that, mostly because I think ‘inflation’ is a made-up concept to keep economists busy. That said, I don’t have a better explanation. It could signal serious cut in household spending, even on necessities, as more households slip into poverty.

Do Poor Neighborhoods Carry More Debt?

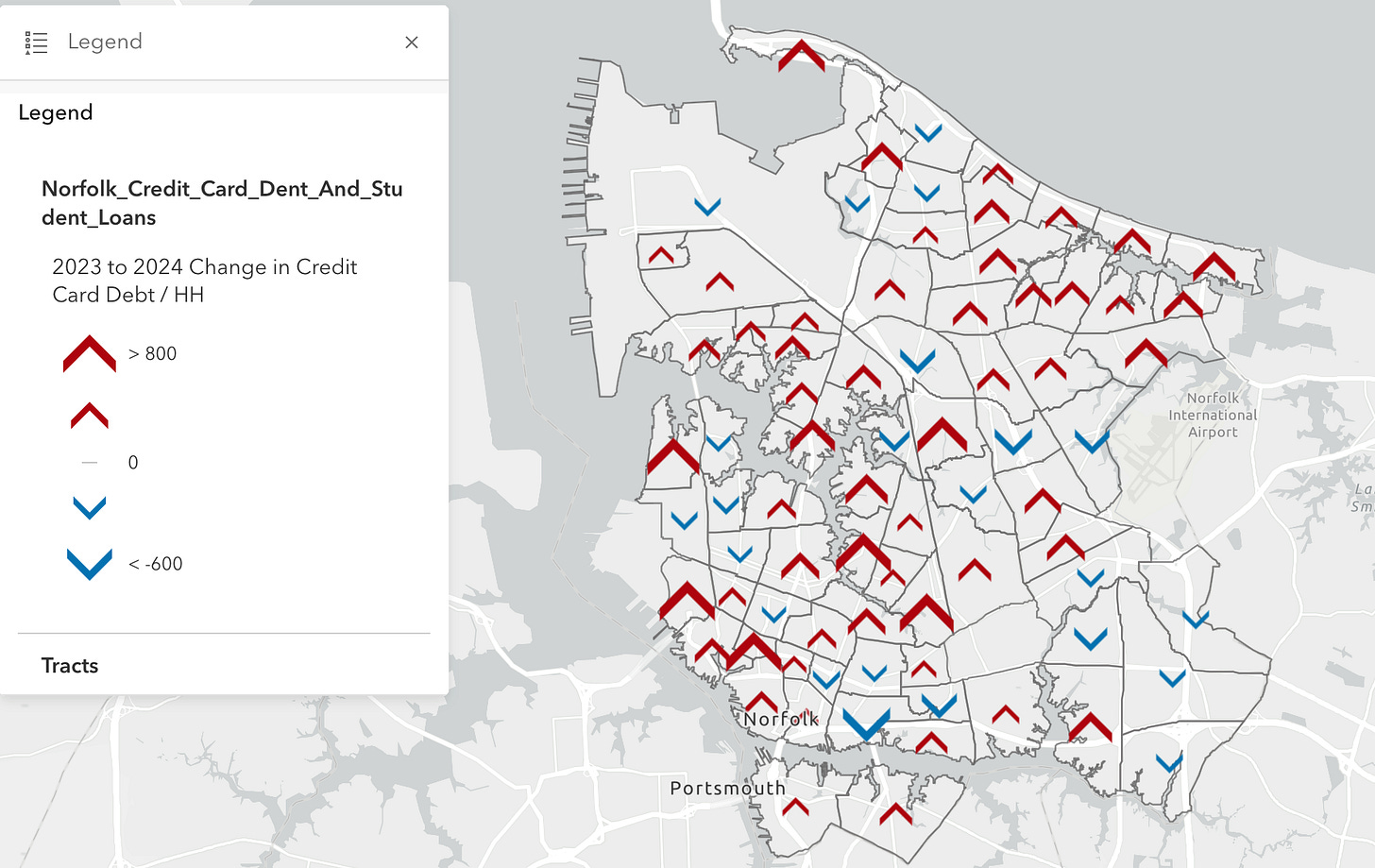

Given the rise in cost of living over the past couple of years, my assumption was that low-income, renter heavy, communities would be seeing the highest jump in credit card debt from 2023 to 2024. Interestingly, the opposite is true.

Zooming in on Norfolk, rather than high-poverty, renter-heavy neighborhoods seeing the largest debt increases, it was affluent, homeowner-dominated, majority-White areas like West Ghent, Downtown, and Lafayette-Winona that had some of the biggest jumps in household credit card debt.

Three key correlations reveal the underlying dynamics:

- Rental prevalence is negatively correlated with debt increases (r=-0.26). High-renter areas (neighborhoods with over 72% renters) saw only about $35 increases versus $240 in mixed-tenure (40-50% renter) neighborhoods.

- Neighborhoods with concentrated poverty were also negatively correlated with debt increases (r = -0.29). Low-poverty areas, with less than 8% of residents in poverty, averaged $332 increases vs. $98 in neighborhoods where more than 20% of the population lives below the poverty line.

- Racial composition had a strong correlation with credit card debt (r = 0.41). Majority-White neighborhoods averaged $315 increases vs. $29 in predominantly non-White areas.

Even when adjusting for income differences and looking at debt-to-income ratios, the same patterns persist, though the correlations weaken somewhat. Low-poverty areas saw credit card debt increases 0.45% of income, compared to 0.19% in high-poverty areas.

The spatial distribution of credit card debt changes in Norfolk is probably reflecting constrained access to financial tools that are open to wealthier households. Higher-poverty and renter-heavy neighborhoods, despite facing greater economic pressures in the past few years (see last month’s post about the permanent recession) were unable or perhaps unwilling to take on additional credit card debt.

Late Fees

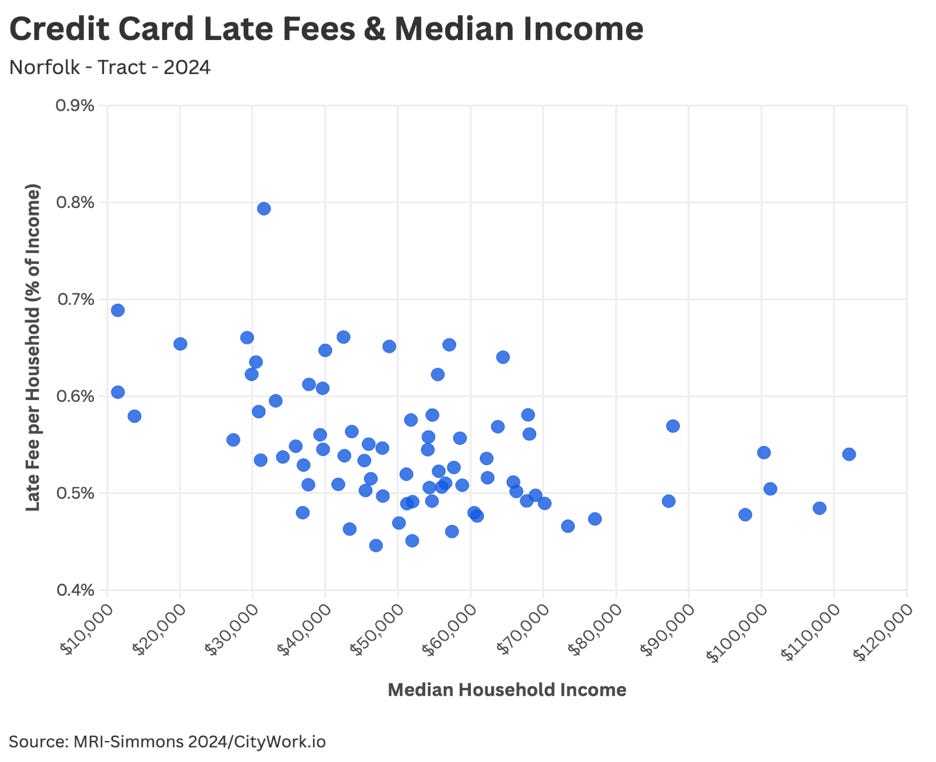

Maybe debt isn't the best measure of financial stress, so what about late fees on credit cards?

Lower-income neighborhoods bear a disproportionately higher burden when it comes to credit card late fees. The correlation between income level and late fee burden shows a moderate negative relationship (r = -0.43), meaning lower-income areas face higher costs relative to their capacity to pay.

Neighborhoods in the highest income quartile pays about 0.52% of income in late fees, while the lowest income quartile pays 0.59%. At the extremes, households in Young Terrace pay nearly 0.8% of income in late fees, while Park Crescent residents pay around 0.4%.

What's interesting is that this data challenges some narratives about “financial literacy” for households in low-income neighborhoods. If higher income meant better financial management, we'd expect much lower absolute late fees. But the relatively small gap in late fees between income groups (0.59% vs 0.52%) suggests that’s not really happening.

Households making well into range of $100,000 a year are paying just as much in late fees as portion of their income as households making $30,000 to $40,000 a year.

There are extremes like Young Terrace and Park Crescent. And affluent households typically have access to more complex credit options, which could be creating more opportunities for late payments. Still, we should think twice before assuming the wealthy got that way just because they were better able to manage their money.

Student Loan Debt

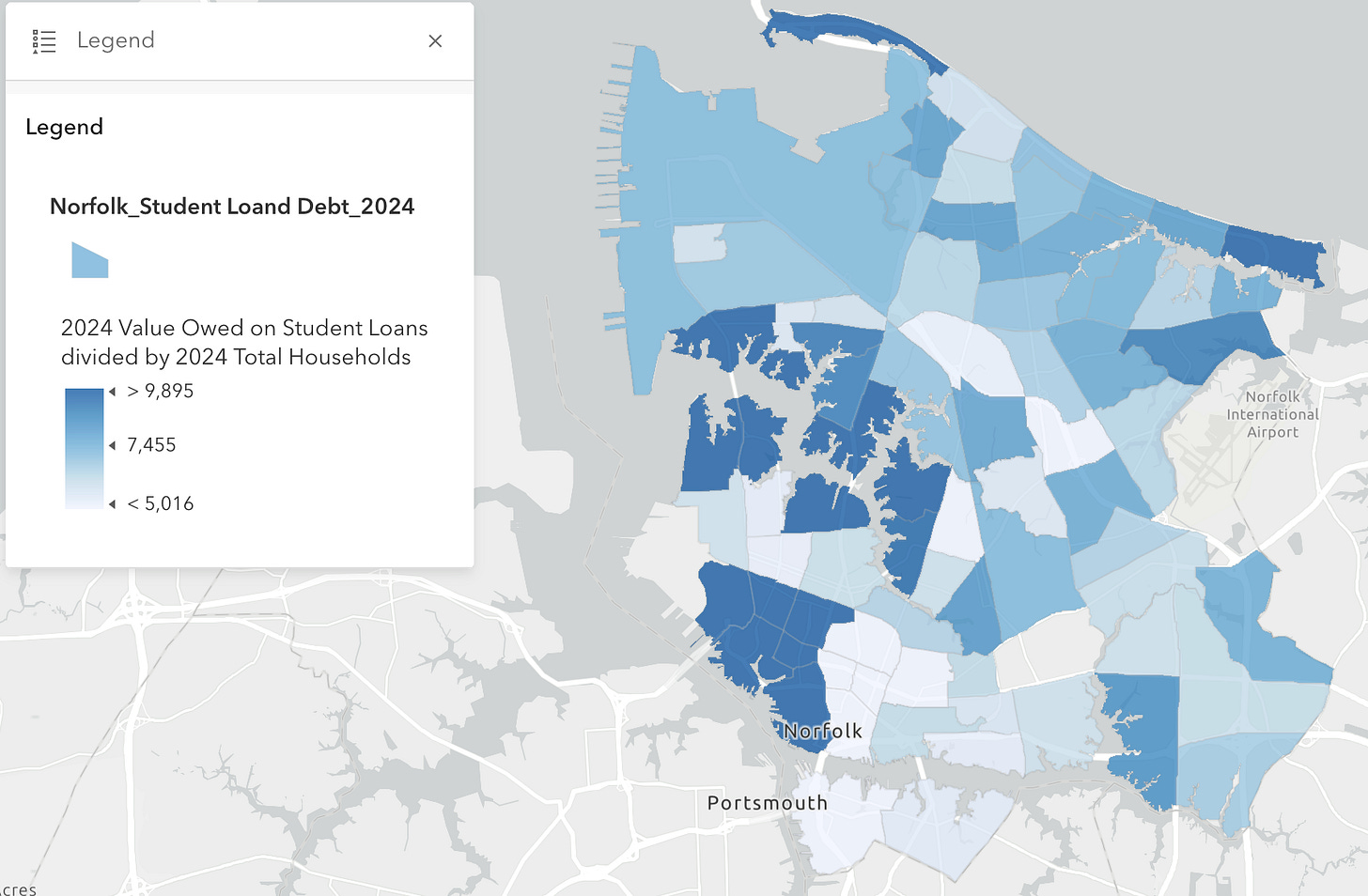

I’ll die with my student loans, and I’ve asked that my remaining balance be inscribed on my headstone. In Norfolk the situation isn’t looking that great either.

In Norfolk, higher-income neighborhoods tend to hold more student debt per household than lower income neighborhoods, in terms of raw dollar amount. Households in the highest income quartile have carried around $10,000 in student loans last year. Households in the lowest income quartile had about $5,000.

The most striking finding is the dual nature of student debt inequality. While wealthier neighborhoods carry nearly double the absolute debt, poorer neighborhoods face a crushing 50% higher debt burden relative to their income. In the poorest 10% of neighborhoods, student loan debt amounts to 18% of household income. Compared to the richest 10% of neighborhoods, student loan debt amounts to 12% of household income.

Wealthier areas have three times more student debt in dollars but are faring much better in terms of being able to manage their loans.

From 2022 to 2024, the wealthiest neighborhoods saw the most significant decrease in student loan debt, with an average reduction of about $1,149 per household. The poorest neighborhoods also saw a drop of about $716 per household. The smallest drop in student loan debt came from neighborhoods making around $50,000 to $60,000 a year, only averaging $433.

The larger decreases in both the poorest and wealthiest neighborhoods could point to how debt relief plans miss a squeezed middle class. However, pandemic lay-offs, and the end of the student loan payment moratorium in late 2023 are also at work here. The poorest borrowers potentially benefited from income-driven repayment plans reaching forgiveness thresholds or qualifying for need-based relief, while the wealthiest had the resources to pay down debt more aggressively. Meanwhile, middle-income neighborhoods may earn too much for substantial relief but lack the income to make a dent in repayment, leaving them in the blind spot of student loan policy.

If only there were some way to cancel the whole thing