Rent numbers are back! After a small glitch in our system we’re back with the latest rental numbers in the region. Plus, we're breaking down who's profiting from Hampton Roads housing.

Overall asking

Average Rent: $1,784.91 | Median Rent: $1,691.00

Studio:

Average Rent: $1,379.66 | Median Rent: $1,396.75

1 Bedroom:

Average Rent: $1,467.32 | Median Rent: $1,492.25

2 Bedrooms:

Average Rent: $1,732.48 | Median Rent: $1,669.50

3 Bedrooms:

Average Rent: $2,115.89 | Median Rent: $2,058.00

4+ Bedrooms:

Average Rent: $2,700.60 | Median Rent: $2,550.00

1. Cashing In

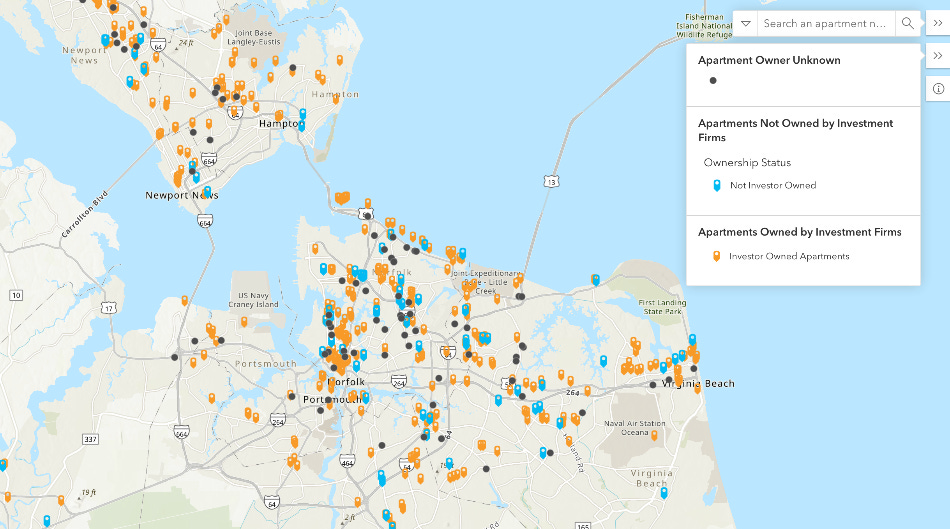

Last month, we released the Hampton Roads Landlord Atlas, tracking the true ownership behind 500+ apartment buildings and 80,000 units. Forty-five percent of Hampton Roads’ multifamily housing is owned by investors. But ownership is only one layer of the story. The Atlas isn’t the answer—it’s the start of the question.

The first question: who’s profiting? It's more than just landlords.

2. Follow the Money

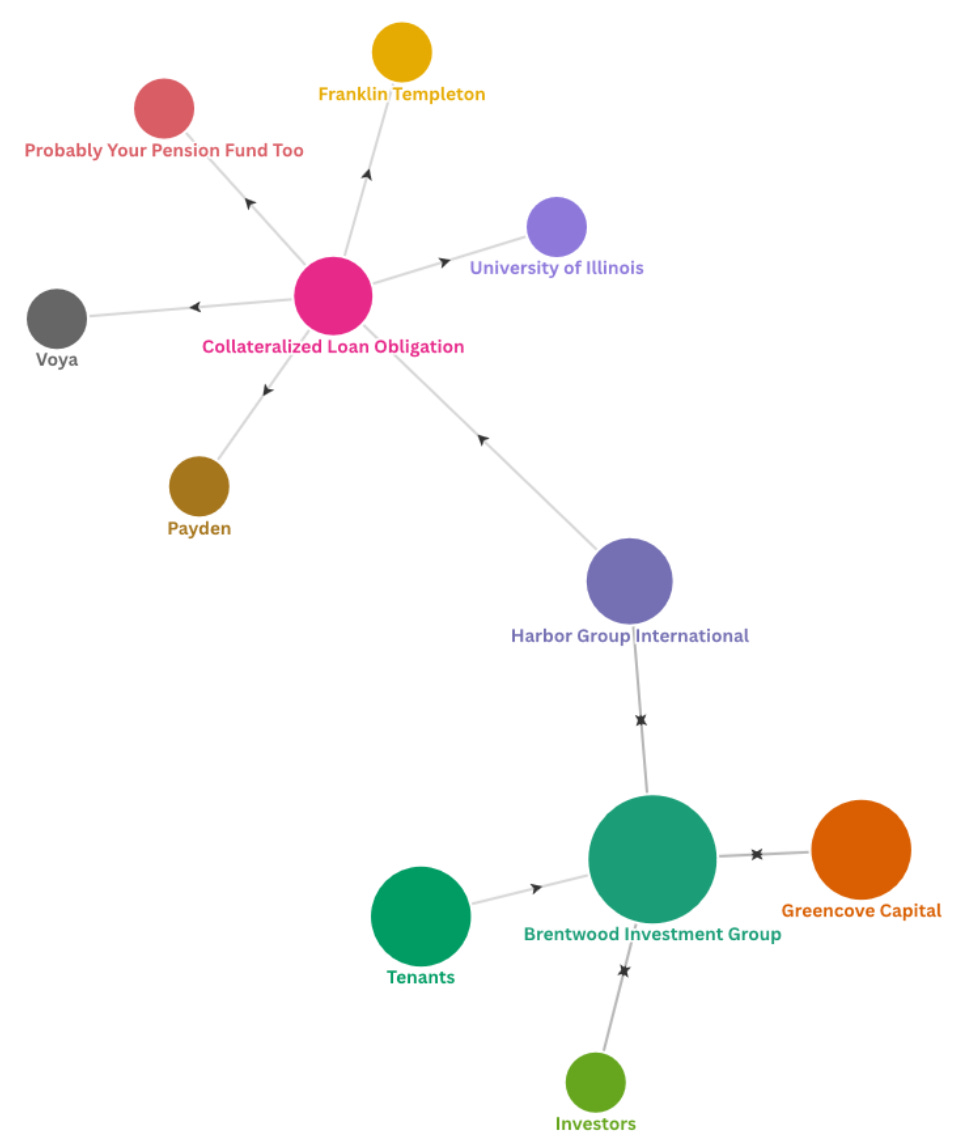

Brentwood Investment Group, or "BIG," a real estate investment firm in New Jersey, offers a prime example of how capital flows through housing—and how the owners aren’t the only ones cashing in.

In 2021, Brentwood teamed up with Greencove Capital to acquire a portfolio of five apartment buildings in Hampton: Cunningham Apartments, Pinewood Apartments, Sacramento Townhomes, Tidemill Farms, and Coliseum Garden Apartments.

At the time, these properties were 98% occupied with “affordable rents” averaging $901 per month—well below the area’s $1,240 average. Brentwood said it spotted a “value-add” opportunity to raise rents by $300 per unit and implement a Ratio Utility Billing System (RUBS). RUBS allows landlords to charge tenants for utilities based on predicted usage rather than actual usage, effectively having renters pay more for utilities without using more.

3. Glass Onion

Brentwood bought the apartments for an “undisclosed amount.” But they didn’t do it with their own money. Brentwood got a $75 million bridge loan from Harbor Group International, one of the world’s largest investment firms headquartered in Norfolk.A bridge loan is a short-term high-interest loan meant to hold investors over as they ramp up renovations, rents, and profit margins. It’s like taking out a payday loan to buy an apartment complex.

Harbor Group then took that loan to Brentwood and packaged it into a Collateralized Loan Obligation (CLO). You can check out our previous report on CLOs, but imagine you have a big box of crayons. Each crayon is a loan given to a landlord to buy an apartment building. Now, imagine we take all these crayons (loans) and put them into a giant crayon box. This big box is our Collateralized Loan Obligation. We then turn around and sell pieces of our big crayon box (CLO) to investors. Every time rent is collected, a little bit goes to the landlord, a little to Harbor Group, a little to the investor that bought a piece of the box.

Harbor Group packaged their loan to Brentwood with 23 other loans and sold it to investors around the world, including Franklin Templeton, Payden, Voya, and The University of Illinois endowment. It's possible your own retirement fund owns a slice of Harbor Group’s CLO, collecting a profit every time the rent is paid.

4. (Almost) Everyone Gets Paid

- Brentwood gets paid from rent hikes and fatter profit margins.

- Greencove gets their slice from Brentwood's profits

- Harbor Group gets paid from interest on the bridge loan, and from fees to investors who buy slices of the CLO.

- Investors who buy the CLO get a piece as rental income goes to pay off the bridge loan.

And the renters?

There have been close to 300 evictions at the properties since Brentwood took over.

Rent hikes and evictions are not the collateral damage of what Doug Henwood called the "theoretical utopia of perfect markets." They are the end notes in a chain of profit and dispossession.