Our rent numbers are back! For good this time 🤞 And we try and divine what a recession might mean for renters across the country and in Hampton Roads.

The average across all units in Hampton Roads was $1,821.26. The median was $1,710

Studio: Average: $1,396.20 | Median: $1,427.00

1 Bedroom Average: $1,583.60 | Median: $1,579.00

2 Bedroom Average: $1,757.66 | Median: $1,700.00

3 Bedroom Average: $2,221.11 | Median: $2,195.00

4+ Bedroom Average: $2,446.73 | Median: $2,297.00

(n=3985)

We make all our data free for the community. Help us out by sharing this post.

What happened to the rental numbers?

We collect rental data by scraping listings across the seven cities of Hampton Roads (we also gather data for Williamsburg too but exclude it since their market is/isn’t part of Hampton Roads). Since listing sites frequently change to block scrapers, we also have to update our code. In this latest update, we added integration-level sanity checks and stronger de-duplication logic to ensure data consistency across scrapes and add more granularity to apartment data.

n.b. Due to these changes, rental numbers going forward should not be compared to earlier data.

Recession Rent

To put it mildly, the last couple of weeks have been among the most significant in the history of finance. There was Black Monday, Bretton Woods, the Lehman collapse, and arguably, Liberation Day. The commentariat is awash with thought pieces about tariff trauma. Few, if any, have asked what this might mean for renters.

History can offer one clue.

Tariff Fallout

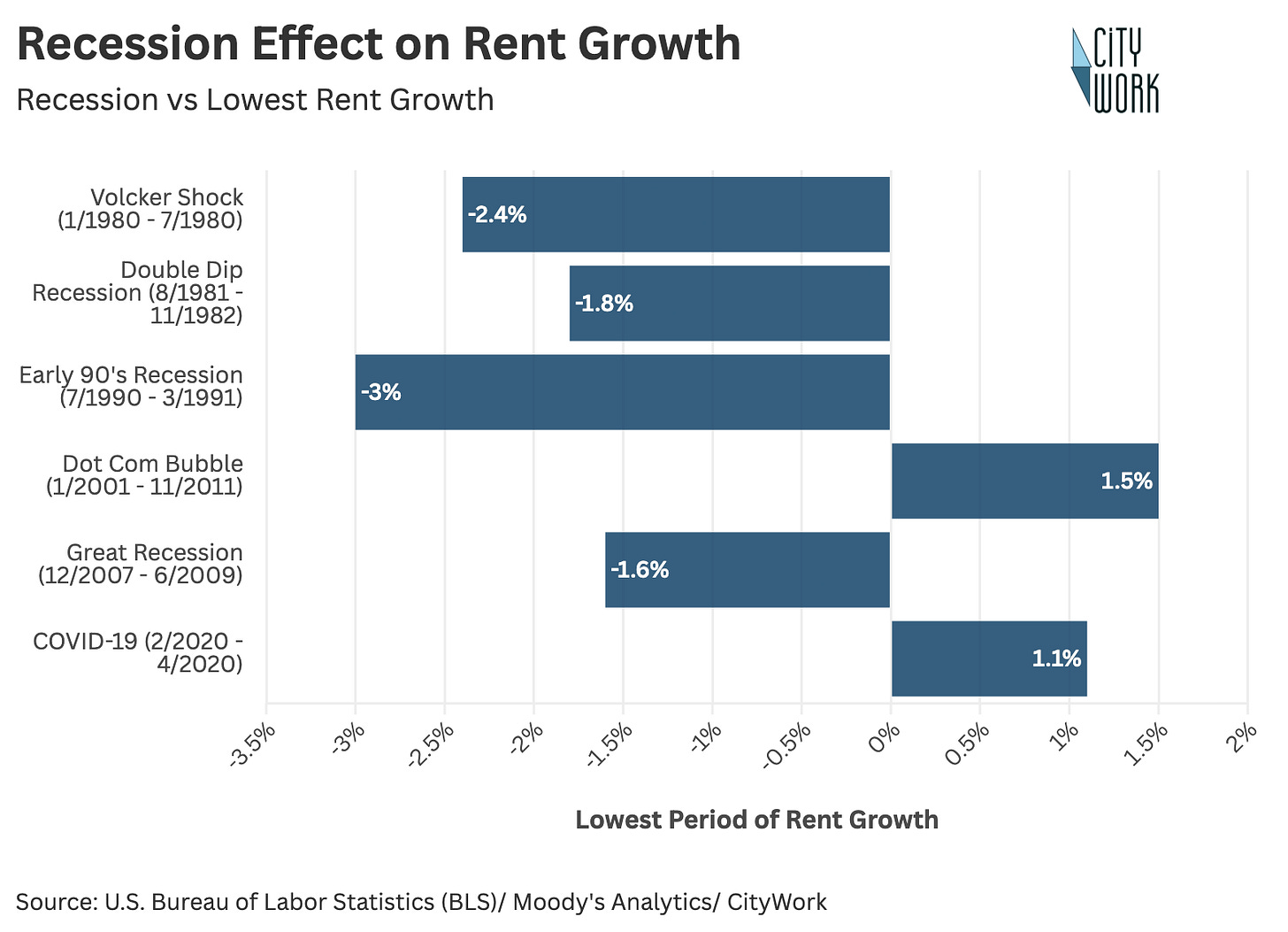

Tariffs can lead to higher production costs, gummed-up supply chains, and a freeze in capital spending. Policy uncertainty can cause businesses to defer hiring or expansion, or lay off workers. A recession, crudely defined as two consecutive quarters of contraction in GDP, is not unlikely. Typically, during a recession, rent growth turns negative but not always.

Nationally, the biggest drop came during the early 1990s recession, where rent growth turned negative by 3%. But that trend is neither universal across recessions nor across unit types. For instance, while rent growth slowed during the Dot Com bust and the Covid-19 mini-recession, they remained positive, with rents gaining over 1% during each recession.

In Hampton Roads, 2020 saw an effective rent growth of 2.5%, way outperforming national growth. And during the 2008 recession, rents in the region remained flat, even as they were contracting nationally. If those two data points are indicative of broader trends, the region’s rents are pretty resilient to recession.

On the one hand, given that this recession is induced rather than structural, we’re likely to see an anemic supply chain whose constraints could slow apartment construction which in turn could cause rents to rise. On the other hand, we are coming out of an apartment building boom not seen in decades, and rents remain stubbornly high. Housing supply and rents are like smoking and cancer. Smoking causes cancer, not smoking doesn’t cure cancer.

Permanent Recession

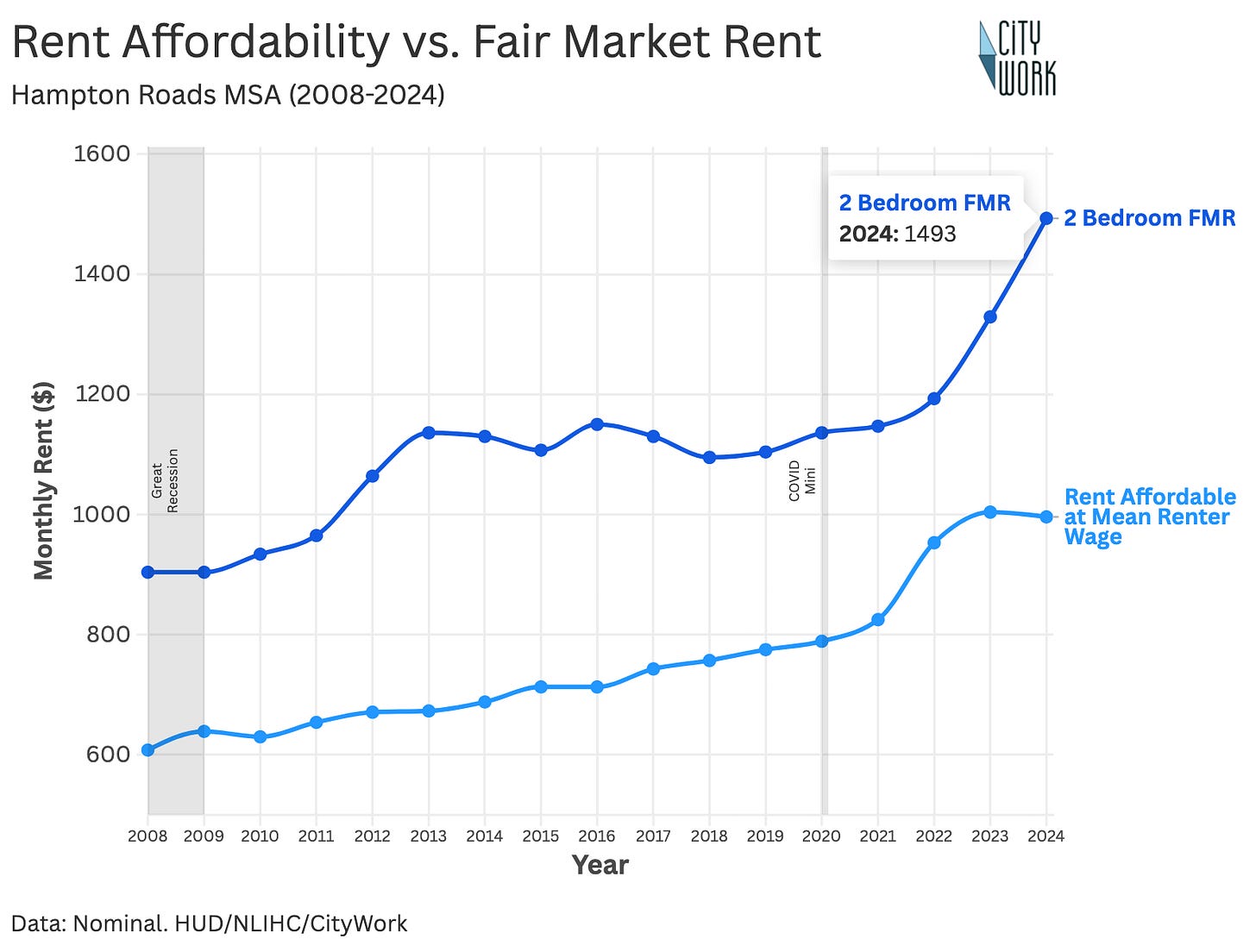

In some ways the question doesn’t matter. Low-income and working-class renters have not been able to find an affordable place to live for decades in Hampton Roads, recession or not. Nationally, 2006 marked the first year that nowhere in the United States could someone making minimum wage afford to rent a 2 bedroom apartment.

In 2008, rents paused while wages inched up. However, renting was still out of reach for minimum wage workers. The 2 bedroom fair market rent held at $904 in 2007 and 2008. This means the affordability gap narrowed slightly by $31, or about 10% from the year before.

Again, that’s not because rent fell, it’s because wages rose slightly. Still, in 2008 a renter still needed 3 full-time jobs at Virginia minimum wage to cover a 2 bedroom apartment.

In 2020, unlike 2008, rents didn’t flinch and incomes rose only a hair, so the affordability gap widened. 2 bedroom fair market rent rose by 2.9% to $1,136 in 2020 from 2019. This means the affordability gap grew by $18 that year.

2008 brought more affordability to Hampton Roads renters. 2020 saw renters worse off. Yet, nothing compared to the gap that emerged in 2024.

What a recession does or doesn’t do to rents is almost irrelevant, because for many renters 2008 never ended. We’ve just been living through the various aftershocks of a permanent recession.

Capital Flight

For my money, which is considerably less at the moment, the more important story here is not about a recession’s impact on housing supply, but on the supply of new housing finance. The past weeks have seen a Sell-America attitude grip markets including once-safe US Treasuries and the dollar.

Why does that matter for renters? Because liquidity for housing is drying up. The firms that finance apartment buildings are suddenly short on cash. Hedge funds that lend to landlords often trade on borrowed money, and when the value of their holdings drops, they face margin calls, essentially demands to top up their cash reserves by selling assets to stay afloat. This is already happening.

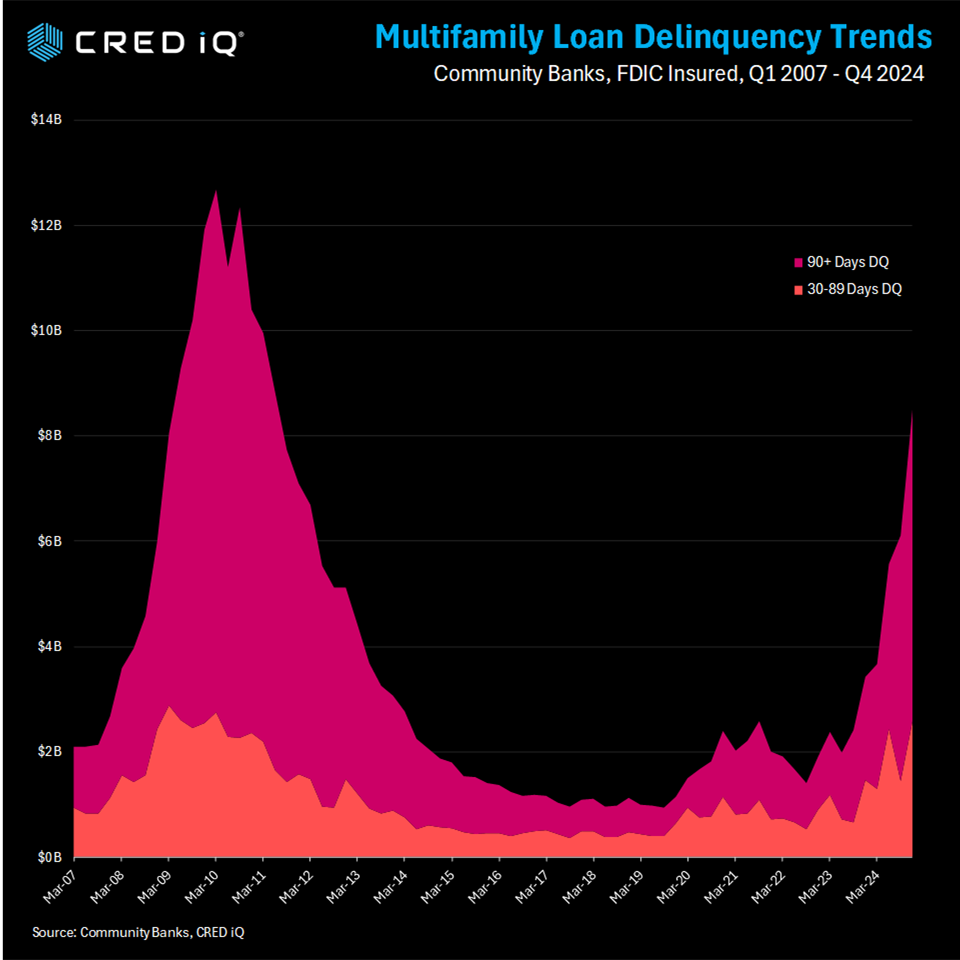

Banks have also pulled back, with multifamily lending now described as “almost non-existent.”

Community banks, the lifeblood of local apartment financing, are under pressure too. As of September 2024, over $6.1 billion in multifamily loans are currently delinquent. Realized losses on apartment loans have reached $504 million, the highest since 2013.

Source: CredIQ

In Hampton Roads, 11% of apartment-related commercial mortgage securities are in distress, ranking us 26th worst in the country. That kind of stress is likely to show up on renters’ monthly bills.

As liquidity dries up, landlords with loans coming due may struggle to refinance. Facing down higher interest rates or tighter refinancing terms may push landlords to:

Raise rents. Higher interest rates or tougher refinancing terms push landlords to pass their added debt costs straight into monthly rent. We’re already seeing this happen, with rents going upas much as $700 a month.

Cut maintenance to preserve cash, as owners may delay repairs or scale back building upkeep.

Aggressively pursue evictions or non-renewals, allowing landlords to remove tenants to “reposition” units to sell to other investors or to relist them at premium prices.

Create artificial vacancies to raise rents. In cities with rent-control or easy lease-transfer rules, owners may find ways to keep units empty until they can legally reset them at a higher market rate.

Some of this is speculation. We’d have more certainty with haruspicy than trying to guess what will happen tomorrow. We don’t know if we’ll be in a recession. And if the Fed lowers interest rates, the story will be much different. Market downturns haven’t really helped renters much in the past, and it’s tough to see how they might in the future.